Subscriptions have taken over consumers’ lives. From streaming services and meal kits to fitness apps and cloud storage, consumers now juggle dozens of recurring charges — many of which they barely remember signing up for. The subscription economy has not just expanded but exploded, and consumers are looking to banks for solutions that put them back in control.

According to a 2021 study, the average U.S. consumer spends over $270 a month on subscriptions, often without realizing it. Services that once required a one-time purchase are now charged monthly or annually. While this model provides convenience and continuous updates, it can also introduce financial ambiguity.

Many people sign up for free trials, intending to cancel before billing starts, but forget. Others subscribe to overlapping services or hold on to apps they no longer use. The result? The average consumer is now spending about $600 per year on unwanted recurring charges, according to a 2021 study from Chase Bank. This is exceptionally shocking, given that two out of five respondents to a 2025 U.S. News survey do not have an emergency savings fund.

Subscription services thrive on inertia. Once a consumer is signed up, companies hope they stay subscribed — not necessarily because they continue to use the product, but because canceling requires effort. This phenomenon, known as the “set it and forget it” trap, makes managing subscriptions a critical consumer need.

But subscription services have taken it even farther than that in their pursuit of profitable growth. Intentionally opaque billing practices, complex cancellation policies and buried terms of service make it difficult for consumers to control what they’re paying for. The crisis has gotten so extreme that the Federal Trade Commission has issued a “click-to-cancel” rule in response to the thousands of complaints the agency has received from consumers unable to cancel unwanted subscriptions.

The subscription service approach has paved the way for a countervailing response: subscription management solutions. Subscription management platforms have emerged as essential financial wellness tools, with direct-to-consumer apps like Rocket Money built to help users track, manage and cancel subscriptions from a central dashboard … for another monthly subscription fee. Rocket Money says it has over 5 million users paying $6 to $12 each month.

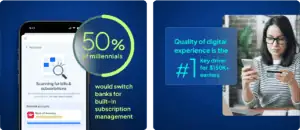

Our own consumer research shows that at least 30% of Americans are paying for a subscription management service, which indicates that bill management may be a compelling account offering. Half of millennials and Generation Z respondents in our 2025 Consumer Banking Sentiment survey say they are willing to change banks to get embedded subscription management services. Indeed, the quality of digital experiences when selecting a primary bank is the No. 1 decision factor for consumers across every generation who are earning $150,000 or more.

This evolution creates an opportunity for banks to help customers achieve better financial outcomes. Subscription management is an important budgeting tool that can save customers amounts that potentially exceed the value of a free checking account or a loan refinance. Adding subscription management capabilities to your premium account services can help your customers budget smarter and align their expenses to their values and needs.

Embedding bill management in your banking app helps customers save on unwanted subscriptions by:

• Algorithmically identifying recurring charges.

• Exposing unused or forgotten subscriptions.

• Tracking and monitoring subscription payment deadlines and renewal dates.

• Alerting users to upcoming milestones.

• Simplifying cancellation processes.

• Negotiating more favorable terms for subscriptions they need.

Subscription models aren’t going anywhere. They’re convenient, scalable and deeply embedded in the way we live now. As more services — think cars, clothing, even pet care — shift to subscription models, the need for robust subscription oversight will only grow. Increasingly, embedded bill management will be a table stakes offering for financial institutions of all types. In this landscape, solutions that help consumers regain clarity and control over their financial commitments are more than useful — they’re essential.