A Model That Worked, Until It Didn’t

Free checking was never free. Overdraft revenue covered account maintenance, and net interest income provided the margin that made the math work. Customers got a no-fee account. Institutions got primacy, deposit volume and a relationship anchor that fed cross-sell for years.

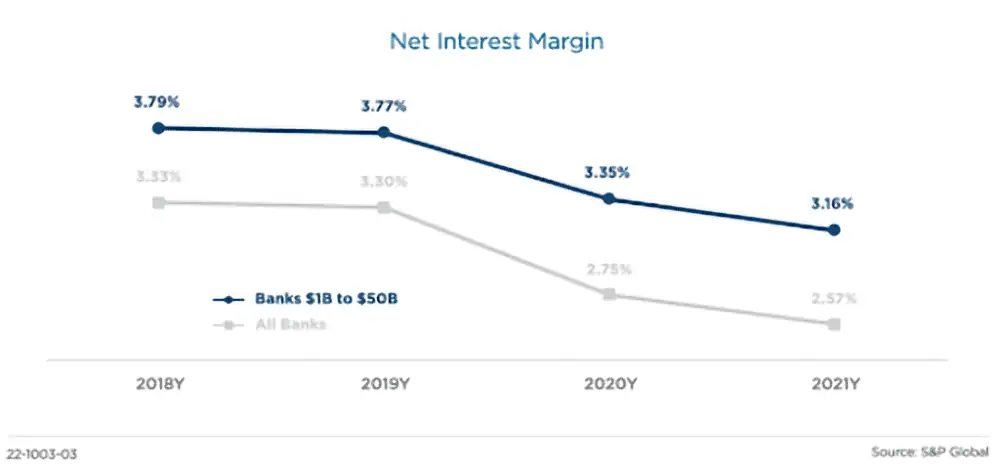

That math has structurally changed. Checking fee income has declined 35% since 2018. Overdraft revenue faces sustained regulatory scrutiny and is unlikely to return. Research from Cornerstone Advisors shows net interest margins compressed through a rate environment that rewarded deposits.

Where the Relationship Actually Lives

Retail customers have not left their banks. Satisfaction scores remain broadly positive. The relationship has changed shape in ways those scores do not capture.

Since 2015, the share of U.S. households considering a community bank their primary checking home has declined 9 percentage points, according to McKinsey & Co., and the gap is accelerating. Automated savings, direct deposit access and subscription-style financial wellness tools are now baseline expectations for customers under 55.

The result is a customer who is technically primary, but not practically primary. The debit card is linked, the direct deposit lands, but the checking account is not at the center of their financial life. And that position is increasingly easy to displace.

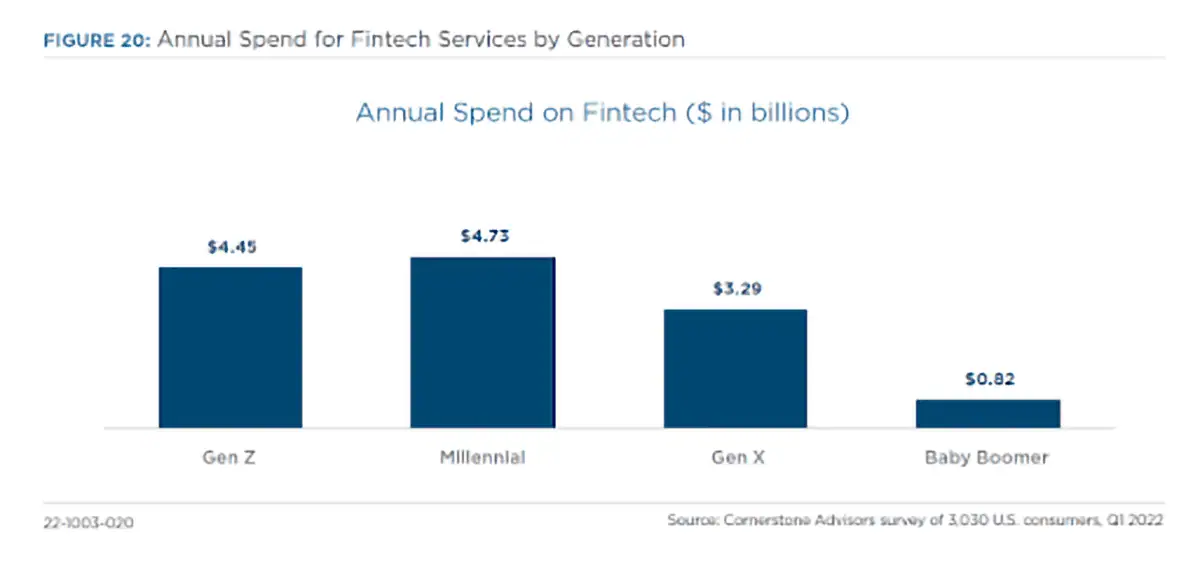

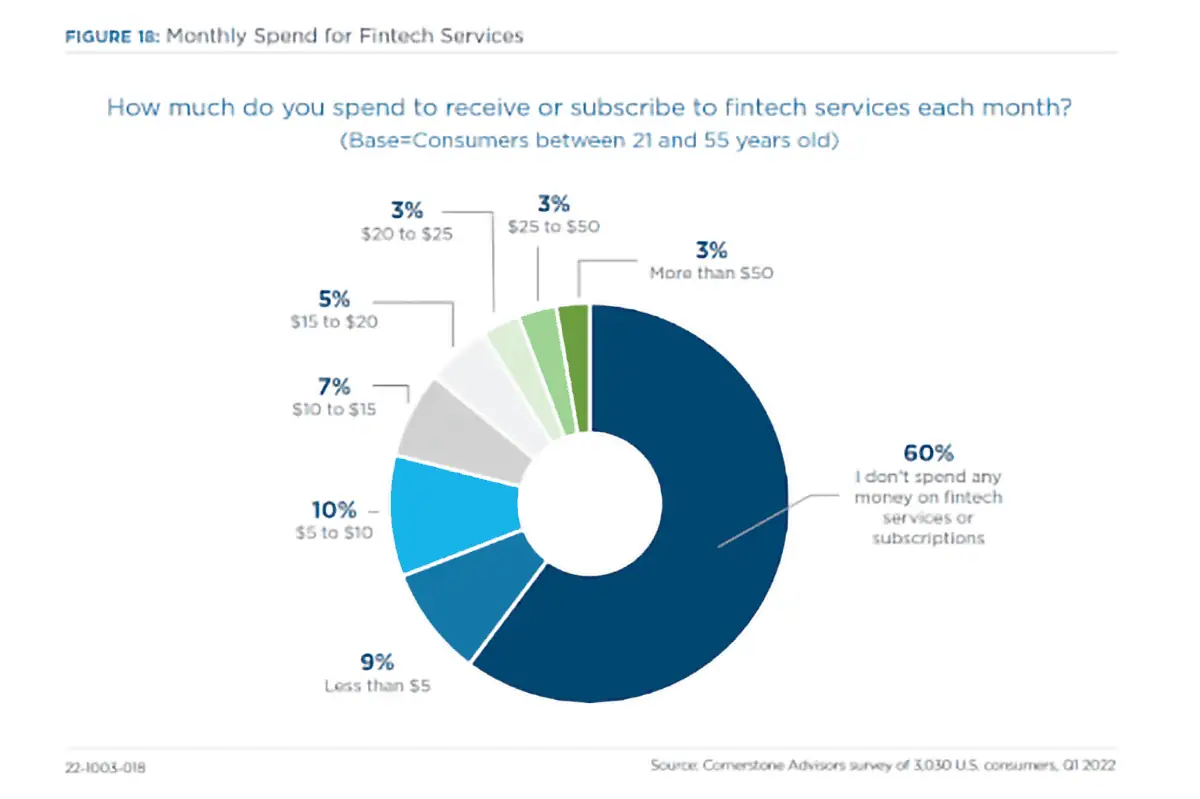

Fintechs have capitalized on exactly this gap. Platforms now capture $13.3 billion annually in subscription revenue from banking customers.

More than 40% of consumers aged 21 to 55 pay for fintech services monthly, half spending $10 or more on benefits sourced outside their primary bank. That is recurring revenue, funded by customers already in a banking relationship and willing to pay for value. It is simply not going to their bank.

Netflix, Spotify and Amazon Prime trained consumers to pay monthly for value. Fintechs applied that to financial services. Banks largely have not.

The Checking Account Isn’t the Problem. The Strategy Is.

The error most institutions make is treating this as a product problem. The checking account itself is not broken, the strategy is — competing on free, reducing friction and hoping the existing relationship holds.

Institutions growing retail deposit share have replaced their checking account’s value proposition rather than defended it. That means bundling tangible, daily-use benefits directly into the account: identity protection, cellular phone coverage, roadside assistance and financial wellness tools. Benefits that make the account earn its place rather than simply occupy it.

The revenue model changes accordingly. A subscription-style checking program funded by customers benefits creates recurring noninterest income that margin compression cannot erode. When the account delivers daily-use value, debit card engagement rises, product attachment improves and relationships consolidate.

Institutions making this shift are seeing checking balances grow 60% or more, per-account fee income replacing overdraft revenue and retention above 95% on upgraded accounts.

Three Decisions Worth Making Now

Audit what your checking account actually delivers. A no-fee account with no compelling benefits is competing on free, and free is not a defensible position when fintechs can match it and add services on top.

Rethink what noninterest income looks like. Subscription fee structures that customers choose because the value is evident require intentional product design, not just a new fee schedule.

Measure primacy by engagement, not account ownership. Holding the direct deposit does not mean holding the relationship. The real question is whether your checking account is in the daily financial life of your customer or just in their contact list.

Define your upsell strategy. Institutions that have made value-added checking work are using it as the foundation for a broader product relationship — moving engaged checking customers into loans, savings and advisory services at meaningfully higher rates than cold acquisition.

The Window Is Open

Banks and credit unions have structural advantages no fintech can replicate — existing trust, regulatory credibility and local presence. Those advantages create a head start for institutions that pair them with a product strategy that earns daily relevance.

The window is open because most institutions have not moved yet. Rate chasers were the first cohort to test institutional stickiness, and many left. Retention of those who stayed depends on what the checking account does for them now, not what it represented five years ago.

The checking account is the anchor, and institutions that use it to build a deeper relationship will already be the center before displacement becomes a question.